This article is an overview of the apartment purchase process. It is not intended to replace the guidance and services of an agent or a lawyer, but may help with some of the preliminary steps involved in buying an apartment in Israel.

Finding an Apartment

Despite the cost, it is often worthwhile to use an agent. They may present properties that one would not have found otherwise. Additionally, a good agent’s negotiations on the buyer’s behalf can sometimes yield better terms than they could have gotten on their own. In this way, an agent is often able to save the buyer a sum close to or even equal to the fee he charges.

Real Estate Agent (Metavech/Tivuch)

An agent will present potential buyers with different properties available and explain the options. Agents in Israel typically charge 2% of the sale price plus VAT.

Customers may attempt to negotiate this amount prior to making a purchase, especially if the purchase price is high.

Purchase Contract

If one is considering purchasing a new apartment, see the section on New Apartments below.

Lawyer

Before signing any papers or committing to any sums, it is crucial to find a good lawyer who can negotiate the terms for you.

In Israel, it is not uncommon for the buyer and seller to use the same lawyer, as it is cheaper and simpler. However, it may be worthwhile to use separate lawyers, since a lawyer working for both the buyer and seller cannot necessarily represent both parties’ best interests.

Zichron Devarim (Principle of Understanding)

A zichron devarim is a binding document without many of the important details included in a full contract. Very often, a party who is anxious to close a deal will suggest signing a zichron devarim. In most cases, it is strongly recommended not to sign a zichron devarim. If there is a real need, it should be done in consultation with a lawyer who can explain the damages that can possibly result. Once a proper zichron devarim is signed, it is equivalent to a full-scale contract with many of the responsibilities, but not all the protections, included in a contract. The buyer’s needs may not be spelled out, and cancellation could result in hefty fines for breach. It may even be tantamount to a contract, which cannot be altered.

Purchase Contract (Chozeh)

The lawyer will prepare the chozeh (purchase contract). The chozeh must be written extremely carefully. Just one incorrect word could cost hundreds or even thousands of dollars. One’s lawyer is there to protect them and can negotiate on their behalf, but ultimately the terms and conditions are decisions which the buyer needs to make. Therefore, make sure that every sentence is understood, and don’t be afraid to comment or question.

The contract must include every minute detail relating to the apartment, the payment schedule and the transfer of property. Make sure that the contract includes the condition of the apartment and whether furniture, air conditioning, etc. are included in the sale. If there are other issues, such as water damage (retivut) or illegal additions made to the apartment, they should also be clearly addressed in the contract.

Payments

Arranging a Payment Schedule

One is entitled to negotiate a payment schedule that suits their needs.

Common payment terms are as follows:

- Usually, a down payment of 10% of the total cost is paid at the time the contract is signed. This is done only after the lawyer verifies that there are no liens on the apartment and that the apartment is really registered in the seller’s name.

- The next payment goes toward paying the seller’s mortgage, if applicable. The down payment must be paid in full before the bank will release any funds from the mortgage. The amounts and dates of each payment are included in the contract.

If the money for one’s payments is coming from overseas, the most cost-effective way to transfer the money to Israel is through a wire transfer — either to your Israeli bank account or through a money changer. The total fees range from 0.6% to 1.5%.

If an American citizen has more than $10,000 at any given point throughout the year in an overseas bank account, he is legally required to file an FBAR with the IRS.

Taking a Mortgage (Mashkanta)

It is worthwhile to apply for a mortgage even before finding an apartment, because it takes time to get approved. Details, including the amount of the mortgage, can easily be changed once an apartment is found.

The process may be long and harrowing, but does not have to be done on your own. A mortgage broker can put one in touch with top lawyers and real estate agents and negotiate the best rates for them. Investing in a professional broker who can do all the legwork will cost more initially, but will likely pay for itself by saving the buyer large sums of money in the long run.

General Guidelines

There are exceptions to almost every rule!

- One will need to show proof of an income at least three times the anticipated monthly mortgage payments. This is because banks want to be sure you can repay your loan. Someone with insufficient income can often be approved on the basis of a co-signer. Some banks may accept foreign co-signers.

- One can borrow up to 70% of the property value. Under certain circumstances one might even be allowed to borrow more. The property value is generally determined according to either the purchase price or the appraised value, depending on which is lower.

For someone who is not a resident of Israel, the law allows them to borrow only 50%.

A non-Israeli resident of Israel (i.e. members of Bituach Leumi) should be allowed to take a mortgage like an Israeli resident. A mortgage broker with experience dealing with foreigners may be able to assist in obtaining the higher rate.

- If one is planning on doing renovations on the property at a later stage, it is possible to get an additional loan. However, interest rates are not as favorable for renovation loans as they are for purchasing a property. In the long run, one can save money on interest by initially borrowing more for the purchase, and then using their own money for renovations.

- It is possible to set up a mortgage in the same currency as one’s income. Israel has a wide range of loans up to 30 years in foreign currency, at both fixed and variable interest rates.

- Every bank has its own unique benefits, as does each type of mortgage. A broker can assist in helping obtain the best loan for the specific buyer.

- If one is considering purchasing a home from a contractor, and is concerned about paying the rent on their current apartment in addition to a mortgage while the new apartment is under construction: request information from the bank about grace chelki (partial grace period) or grace malei (full grace period), which allows the buyer to pay less or even none of the mortgage until the apartment is ready.

Documents Needed at the Bank

- Teudat zehut for the buyer and their spouse if relevant; for a non-israeli, two photo identifications for each spouse, i.e. passport and driver’s license.

- Bank statements from the last three months.

- Proof of income — for foreigners, two years of tax returns are required.

- A credit score or report for foreigners — required by some banks.

Other Expenses

Other expenses are incurred over the course of buying a property. Following is a rough estimate of the additional costs involved.

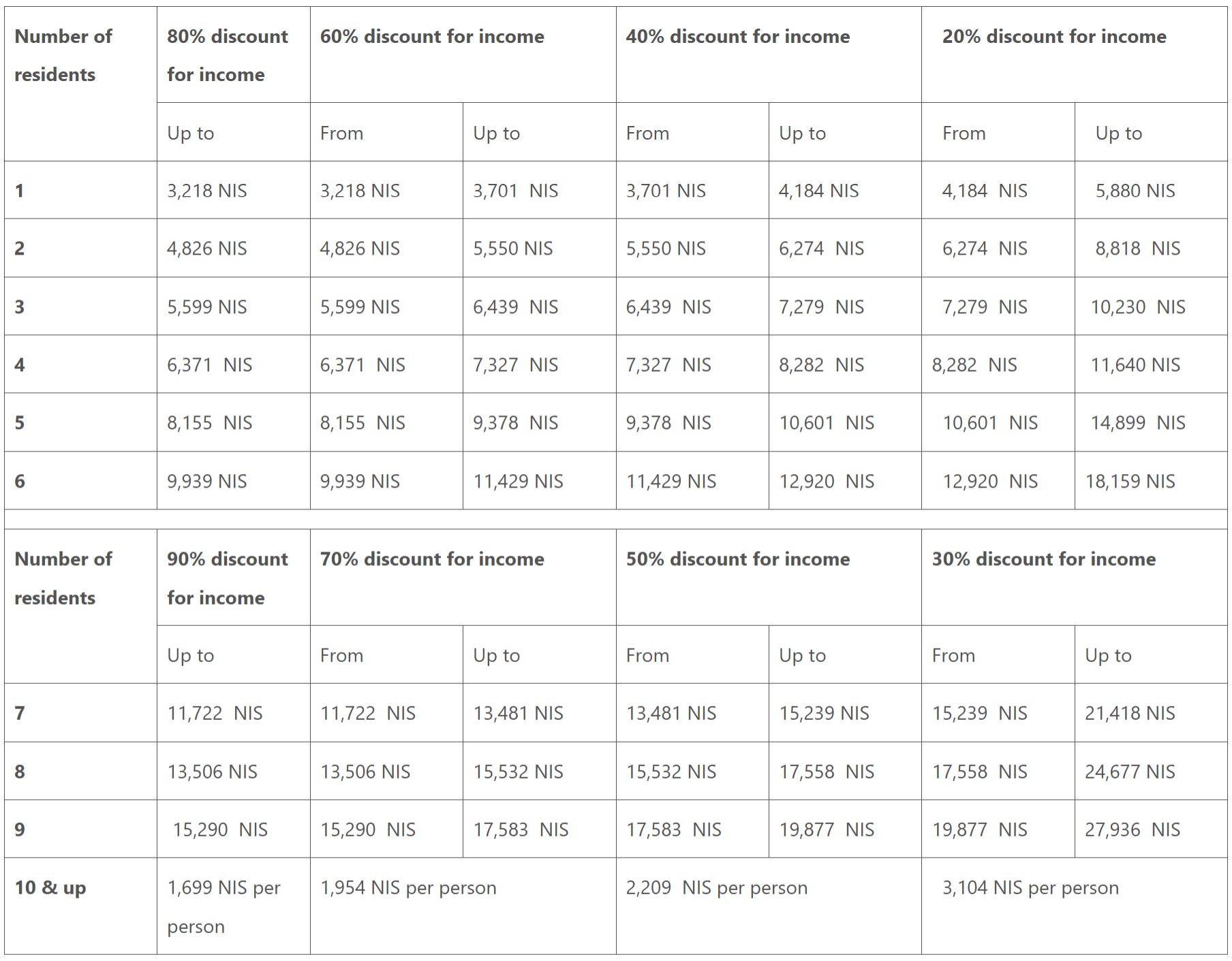

- Mas rechishah (purchase tax)- the purchase tax rates formula is complicated, and the percentage rises in relation to the purchase price. A recent oleh (new immigrant), a newlywed, disabled individual, or a first-time homeowner can receive a substantial discount on this tax.

Foreigners pay a higher rate of mas rechishah. However, foreigners who can prove that they are residents whose center of life is in Israel may be entitled to pay mas rechishah like an Israeli. An experienced lawyer should be able to assist with this.

- Real estate agent commission- approximately 2% + VAT

- Lawyer fees- generally vary between 0.25% and 1% + VAT.

- P’tichat tik (mortgage processing fee)- generally between 0.25% and 0.5% of the loan.

- Property appraisal fee- before getting approved for a mortgage, the bank stipulates that the property must be appraised by a shamai (appraiser). The cost of this appraisal differs by bank, the amount borrowed, and the property value. Some people prefer to appraise the value of their property even before starting with a mortgage. Hiring a private appraiser costs around 4,000 NIS.

When hiring a private appraiser and planning to take a mortgage, be sure the appraiser is approved by your bank.

- Additional charges, including registration fees paid to the Land Registration Office. approximately 1,000 NIS.

Registering Ownership

There are three categories of registration of ownership:

- TABU

- Minhal M’Karkai Israel (Israel Lands Authority)

- Chevrot Meshaknot (Land Management Companies).

A lawyer will generally deal with this matter and can explain the ramifications of the different ownership options.

A Note On New Apartments and Contractors

New apartments are generally sold directly by contractors.

In the case of a new apartment, investigate whether there is proper licensing for the contractor and his project. Make sure his taxes have been properly dealt with and that he has the proper building rights if he has entered a “combination deal” with landowners.

If one is planning to take out a mortgage, the bank will require documentation of all the above.

Before making a decision, it is critical to get bank guarantees and check out projects or buildings that the contractor has built in the past.

One has the legal right to receive technical plans of the apartment and the building in which it is to be built. One also has the legal right to show the plans to professional engineers, architects and an attorney.

Often, contractors will try to demand that you use their lawyers. However, it is very difficult to make any changes to the contract or to negotiate any details of the sale without one’s own personal lawyer. It is usually worth the extra expense of a private lawyer so that the buyer has a say instead of signing based upon the contractor’s lawyer’s decisions.

One is entitled to make changes to the proposed contract, and changes can be made — even if the contractor claims at first that they cannot.

Unlike in the case of secondhand apartments, matters such as parking spaces, solar heaters, development, gardens, water, gas and electric connections, as well as public ownership between neighbors, taxes and repairs, must be specifically agreed upon.

When buying an apartment through a contractor, one is obligated to pay only according to the progress of the building. The terms of payment are set by the bank offering the guarantee or the lawyer signing ne’emanut (an escrow account; another form of guarantee, as mentioned above). This is not just a negotiating pawn — it’s the law.

By law, nothing should be paid unless the contractor provides a bank guarantee (arvut banka’it) or a similar guarantee.

The payment schedule is generally as follows:

- When the roof, or first floor of the building not on pillars, is finished: pay up to 40%.

- When the frame (skeleton), including the walls, is finished: pay another 20%.

- With the outer plaster: pay another 20%.

- Upon receiving the key: pay the last 20%.